(Click on heading to leave a comment at bottom of page)

The drums are beginning to throb. I have been hearing more voices in the last few weeks talking about inflation, so much so that I’ve started to think about what may be ahead. ‘Respected’ figures in different countries such as Bank of England policy maker Catherine Mann have dismissed the current acceleration in global inflation as a threat, describing it as ‘transitory rather than troubling’ and thereby justifying ultra-low interest rates and flooding the economy with paper money to service government debt. Of course ‘transitory’ has no fixed timeline – thereby making the adjective meaningless in this context.

History is full of examples of inflation destroying economies and destroying lives. We don’t need to go back far. I can personally remember inflation in the UK soaring in the 70s and 80s such that the Bank of England interest rate rose to 15% in 1989 to try to choke off inflation. In the USA, inflation reached 14% in 1980. Nixon wanted monetary policy to support massive budget deficits and the end result was inflation that destroyed businesses and lives – even John Connally, the Nixon-installed Treasury Secretary (who had no formal economics training) later declared personal bankruptcy.

I take the comments from central bankers such as Catherine Mann with a pinch of salt because it is in their interest to encourage inflation. Let me repeat that, it is in their interest to encourage inflation. It is also in their interest to keep interest rates low, which will, in turn support increasing inflation.

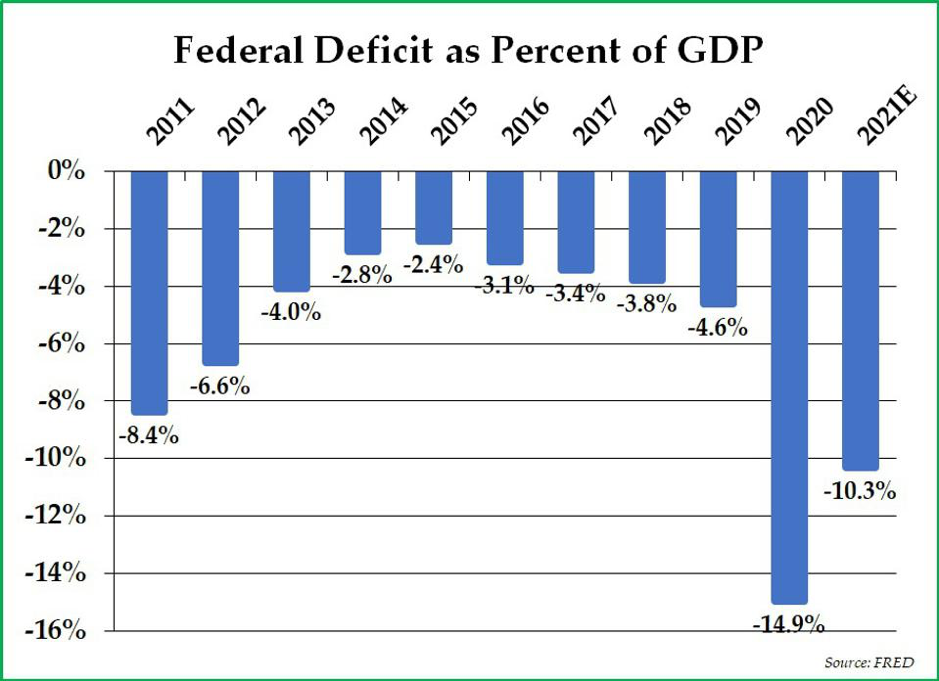

With the pandemic of COVID we have seen governments around the world take the goves off and run huge deficits funded by government debt that will have to be serviced and repaid (I say ‘huge’ but if Nixon’s budget deficits can be described as ‘massive’ perhaps I should say gargantuan).

Why? If interest rates rise they will have to replace cheaper debt coming due with more expensive debt, plunging them further into debt. Inflation however means debt worth 100 today is worth less than 100 when it comes due, so the greater the inflation, the easier it becomes to pay down debt.

In the last few weeks I have been reading about the disaster unfolding in the UK thanks to the self-inflicted wound of Brexit compounded by a buffoon of a leader and an incompetent and corrupt set of hangers-on. It is hardly the backdrop for effective economic management. In the US we have also seen a massive inflationary boost with tax giveaways mostly to those who did not need it and tariffs under Trump and the coming tidal wave of an unfunded multi-trillion dollar spending spree under Biden. And these are two supposedly ‘well-managed’ economies. Let’s not even look at South Africa, Belarus, Brazil etc. etc.

I think it’s inescapable – we are heading into a sustained inflationary period. I’m looking afresh at my own financial planning as a result.

If history should be a signpost to the future, economic management should perhaps be its greatest beneficiary as it is fundamentally the process of balancing supply and demand and creating a framework for the financial well-being of citizens.

However, as is so often the case, it hasn’t quite worked out that way because the political push for power distorts everything.

The post The Coming Inflation first appeared on David Cairns of Finavon.